Medigap Plan G is one of the most common Medicare Supplement plans offered under the Medicare Supplement standardized plans. You can view the complete standardized chart here:Medigap coverage chart. Plan G is a smart alternative to Plan F in most cases. This is because the premium savings typically offset the Medicare Part B deductible, which is the only difference in benefits between these two Medigap plans. Also, Plan G is historically more rate-stable than Plan F and other Medigap plans that are offered on a “guaranteed issue” basis. On average, people who have Plan G are healthier because companies are not required to issue them coverage under than plan if they are losing employer coverage or Advantage plan coverage.

{kind=link}

Why Choose Medigap Plan G

- It is a less expensive alternative to the commonly-promoted Plan F. It is the 2nd most comprehensive of the commonly-offered Medigap plans.

- It allow you to have predictable, stable out of pocket expenses. At the start of the year, you can budget for health care expenses by simply multiplying the premium by 12 and adding the Medicare Part B deductible.

- The premium savings gained under Plan G generally is greater than the Medicare Part B deductible, and that is the only difference between Plan F and Plan G.

- A Plan G from any company can be used at any doctor/hospital nationwide that takes Medicare. There are no network restrictions (as there are not on any of the Medigap plans).

- All companies offer the same standardized benefits on Medigap plans. A Plan G with one company is the exact same as a Plan G with another.

- Plan G benefits will never change. The coverage is “guaranteed renewable”. Once you sign up for a plan, it will not change benefits on an annual basis.

- Medigap G is historically more “rate-stable” than many other plans. This is because it is not offered on a “guaranteed issue” basis like some of the other plans. This means that people who have Plan G can be thought, on average, to be more healthy than those on some other plans, like Plan F.

What Does Plan G cover?

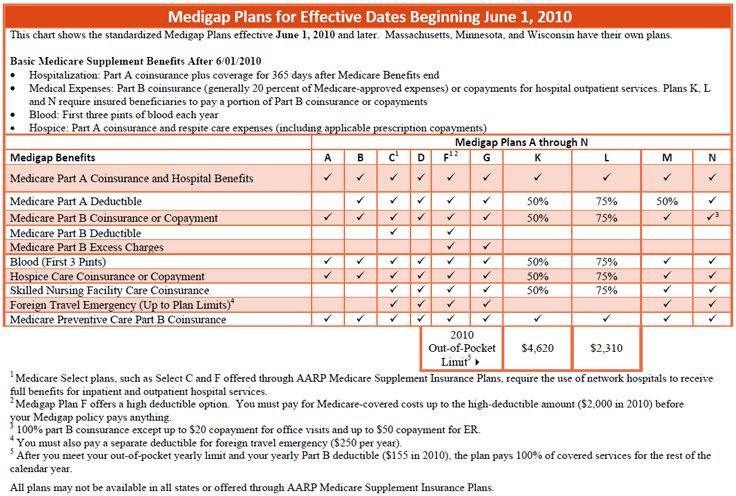

The first step in doing a Medicare Supplement comparison is to understand what each plan covers. This is easier than you may think, simply because Medicare has standardized the plans. Each company is required to offer plans straight from the Medigap coverage chart, which shows exactly what each plan covers. Below, you will find a summary of benefits for what Plan G covers:

- Plan G covers “Basic Benefits”. This includes 100% Part B coinsurance. Additionally, “Basic Benefits” also encompasses the Part A coinsurance (which is the 20% that Medicare doesn’t cover), plus it covers you for an additional 365 days after Medicare benefits end.

- Blood – Plan G, just like other supplement plans, covers the first three pints of blood each calendar year.

- Hospice – Plan G covers the Medicare Part A coinsurance (this is the 20% that Medicare doesn’t pay) for these services.

- Skilled nursing facility coinsurance. This plan covers the 20% that Medicare doesn’t pay at a skilled nursing facility.

- The Medicare Part A deductible. For 2013, this deductible is $1,184/benefit period. The Plan G covers this deductible, but it does not cover the Medicare Part B deductible, which is the smaller of the two deductibles ($183/year for 2017) and one that several of the Medigap plans do not cover.

- Part B Excess charges. Although these are not a frequent occurrence, they can occur if a doctor doesn’t accept the Medicare-approved amount. The plan picks up those excess charges, so you do not have to pay them if your doctor charges more than the Medicare-approved amount for a service or procedure.

- Foreign Travel Emergency. Plan G also covers medically necessary emergency care services. This begins during the first 60 days of each trip outside the USA. As part of this benefit, there is a separate $250 deductible on these charges and a $50,000 lifetime limit.

How Does Medigap Plan G Work?

The Plan G works just like other Medigap plans do. Under this plan, you can go to any doctor or hospital that takes Medicare nationwide. There are no network restrictions, like on the other Medigap plans. Your Medicare Supplement plan is tied to your Medicare, and claims are paid through the Medicare “crossover” system. You do not have to manually file claims – they are handled automatically by Medicare and the insurance company. With Plan G, you are responsible only for the Medicare Part B deductible, which the plan does not cover. This deductible is $183/year for the 2017 calendar year. Other charges, including the Medicare Part A deductible and the Medicare coinsurance amounts, are covered by the plan, so they are not your responsibility.

Where Can I View the Benefits of Plan G?

The standardized plans chart dictates what Medigap plans cover. This chart is Federally-published and Federally-mandated. You can view the chart here: Medigap Coverage chart.

The Medigap coverage chart shows you which Medicare Supplement plans cover which things, so using the chart, you can easily compare between the various Medicare supplement plan offerings and see which plan is the best fit for you.

Frequently Asked Questions about Plan G

Benefits for Plan G are Federally-standardized and they are spelled out on the Medigap coverage chart; however, you may still have questions about how the plan works or what it covers. Below, we’ve addressed some of the most frequently asked questions about the plan:

- Are there certain time periods during which you can enroll in a Medigap Plan G?

Contrary to popular belief, you can enroll in ANY Medicare Supplement plan at ANY time – there are no specific annual enrollment periods (like there are with Medicare Part D and Medicare Advantage plans). However, you will find that there are certain times that are more advisable for enrolling into Medigap plans. The most significant and common time to enroll in a Medigap plan is the Federally-mandated “open enrollment” period that everyone is given surrounding their 65th birthday or their enrollment in Medicare Part B. This is the optimal time to enroll in a Medicare supplement plan without having to answer any medical questions or worry about pre-existing conditions.With all companies, this period lasts for 6 months and begins on the first day of the month that they are both age 65 and enrolled in Medicare Part B. Also, you may qualify for a “Guaranteed Issue” period if you are in certain situations, including but not limited to, leaving/losing employer coverage, losing a Medicare Advantage plan coverage, or leaving a plan’s service area. To get more specifics and/or to find out if you are in one of these periods, please contact us using our website – Medicare Supplement. - So, if coverage is the exact same, why are rates different?

- So, How Can I Compare Rates from Multiple Companies for Plan G?

To get a rate quote comparison from us, simply request the information online using: Medicare Supplement Quotes. We can provide the information you are seeking so you can compare multiple quotes in a centralized place.