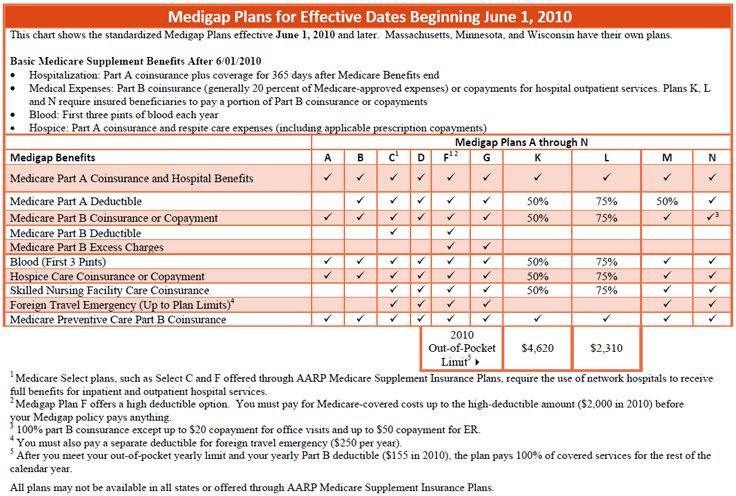

Medicare Supplement insurance plans are plans that are designed to go with “original” Medicare (Parts A & B). These plans are Federally-standardized – all insurance companies have to offer the same coverage plans, so there is no difference in coverage from one company to another. You can view the chart that all companies must go by here: Medigap Coverage Chart

Because the plans are the same, it is easy to compare Medigap (another name for a Medicare Supplement – those two terms are interchangeable) plans from different insurance companies. You can easily compare “apples to apples”. For example, a Plan F; with one company is the exact same as a Plan ‘F’ with another company.

This makes reducing your premium on an existing policy or choosing a supplement plan extremely easy to do! There are four simple steps to follow when comparing Medicare Supplements.

Step 1. Understand the Basics

Here are a few very important things that you should know about Medigap insurance, if you are turning 65 or comparing plan quotes or options:

- Medicare Part A does not, generally, have a premium, but there is a premium that you have to pay (usually comes out of your Social Security check) for Part B.

- To get a Medicare Supplement, you MUST have both Part A & Part B.

- You pay a premium to the Medigap insurance company.

- Medicare Supplement plans are the same from company to company, so price is the primary differentiating factor. They go by this plan chart (Medigap Coverage Chart).

- All supplement plans pay using the Medicare “crossover” system. You do NOT have to file claims for any supplement plan.

- All supplement plans allow you to go to any doctor or hospital that takes Medicare – there are NO networks.

- Medigap plans are “guaranteed renewable” meaning that your insurance company cannot cancel you unless you do not pay the premiums.

- Medigap plans do NOT cover prescription drugs. You have to get Medicare Part D in order to have drug coverage. It is the portion of Medicare that covers prescription drugs.

- There are NO annual enrollment periods for Medicare Supplements, contrary to popular belief. You have a 6-month initial enrollment period when you first turn 65 or enroll in Part B. During this time, there is no medical underwriting or health questions. After that time, you can sign up for a supplement or change your supplement at any time; however, you do have to answer health questions.

- You may also want to review the booklet that Medicare publishes. Also, you can visit Medicare’s website to get additional information at Medicare.gov.

Step 2. Get Quotes

Getting Medicare Supplement plan quotes is easy to do. Most people find it convenient and useful to request a Medigap quote comparison online. This way, you don’t have to spend time going to an insurance office, sitting in a presentation, or bringing a “pushy” agent into your home. Whatever you do, you want to make sure of a few things when getting quotes:

- First, you want to get quotes from an agent or agency that deals exclusively with Medicare insurance. Medicare is complex, and agents that work only with Medicare insurance have a better chance of correctly and efficiently answering your questions.

- Also, use an independent agent or agency, if possible, to get quotes. An agent that works with only one company or works “for” an insurance company has a loyalty to that company first, and you second. An independent agent, however, can give unbiased opinions and information, based on their clients’ experiences.

- Be careful about how many times you request information. Generally, requesting quotes from one website will get you the desired results and allow you to avoid getting inundated with phone calls and emails.

- Use correct and valid information. It sounds simple but, if you want accurate information in return, you must use your correct information (i.e. birthday, tobacco usage, zip code, etc.).

- Finally, understand that one agent or agency cannot offer a better “deal” than another. It is illegal for one agent, or agency, to offer better rates for the same company and plan. So, you will not get better rates by going through a different agency or straight through the company.

Step 3. Compare Rates for the Plan(s) you Want

So, now that you have your quotes, what do you do next? The first and foremost thing that you need to decide is what plan you want. As discussed before, the plans are Federally-standardized so there is no variation in what a certain plan covers. However, different plans do vary.

The three most common plans are:

- Medigap Plan F. This is the most common and comprehensive plan. It covers everything that Medicare doesn’t cover at the doctor and hospital so that you don’t have any out of pocket costs.

- Medigap Plan G. This plan is one step below Plan F. It does not cover the Medicare Part B deductible, which is $183/year (for 2017). That, however, is the only difference between those two common plans.

- Medigap Plan N. This is a lower-tier plan that has some cost-sharing ($20 doctor’s office co-pay and $50 emergency room co-pay) in exchange for lower monthly premiums. It is designed as an alternative to Medicare Advantage plans, while still giving you the flexibility and stability of a supplement plan.

There are other plan options as well, and different plans are more common in different areas. But nationwide, these are the three plans that we see as the best and most competitively-priced options.

Once you have an idea of the plan you want, you can easily compare rates on that particular plan. Again, because the plans are standardized and all companies pay claims the same way, you are comparing “apples to apples”. Some differences in the rates may cause you to re-evaluate the plan that you want. For example, if Plan G is $250/year less than Plan F, it would make sense that would be a better option (since the deductible, which is the only difference, is only $183/year).

Another thing that must be taken into account is your health. If you have some ongoing health problems that require many doctor visits a year, for example, you may not want to look at Plan N (since it has co-pays) unless it was your only option.

{kind=link}

Step 4. Make an Informed Selection

Once you have all of the information together, you can easily make an informed, unbiased selection of a Medigap plan that best meets your needs and desires.

Situation: You don’t want to have any co-pays, at all, ever… Plan F is right for you!

Situation: You don’t mind having some out of pocket costs and don’t go to the doctor very much… Plan N is right for you!

Remember: monthly premium rate is the most important factor when deciding between companies!

Once a selection is made, applying is the easiest part. Most companies offer online applications. Or, you can apply over the phone or through the mail. Here is what you should know about selecting and applying for a Medicare Supplement plan:

- Apply Early. It generally takes at least two weeks for a supplement application to be processed.

- Answer the Questions Truthfully. If you have to answer health questions on the Medigap application, answer them truthfully. The company checks your medical records, anyway.

- Keep a Copy for Yourself. Whenever possible, keep a copy of your application for yourself. This always helps if there is a problem or question about something on the application.

- Ask Questions Upfront. It is always best to get all of your questions answered prior to applying for the policy.

- Remember to Cancel Your Old Policy. If you are replacing an older Medicare Supplement, you must cancel your old supplement policy, effective the day your new one starts, to avoid being double-covered (and double-paying).

The Top Five Misconceptions About Medicare Supplement Plans

Particularly at the end of the year, when more people are comparing their Medigap policies, it is amazing to me how many people don’t understand what they have or how the plans work. That said, we realize it can be convoluted and complicated. We certainly don’t have ambition to “correct” everyone’s misconceptions; however, in the spirit of doing my part, here are the top 5 misconceptions that I hear regularly:

- MYTH: You can only change Medigap plans during the annual Medicare enrollment period. TRUTH: This is simply not the case. You can change Medigap plans at any time of the year, for any reason. The annual Medicare enrollment period only applies to the Part D plans and the Medicare replacement plans (Medicare Advantage). That leads me to…

- MYTH: You do NOT have to answer medical questions if you change plans during the Medicare annual enrollment period. TRUTH: Since the Medicare annual enrollment period doesn’t apply to Medigap plans at all, there is no such time of the year that you can be exempt from medical questions for Medicare Supplement plans. The only things that get you “out” of answering medical questions are the valid open enrollment (i.e. turning 65) or “guaranteed issue” (i.e. losing employer coverage) periods.

- MYTH: Some companies, especially if they claim to be “issue-age” or “community-rated”, will NOT go up over time. TRUTH: If only this were true! Unfortunately, there’s no “silver bullet”. All Medigap plans are going to go up over time. The only thing that varies is their reasons for increase.

- MYTH: I need to call my doctor’s office to see if they take this plan. TRUTH: All Medigap plans are accepted, and required to be so, by any doctor/hospital that takes Medicare. There are no networks on Medicare Supplement plans. So as long as your doctor takes your primary coverage (Medicare) they must accept your secondary coverage (Medigap plan).

- MYTH: My Medicare “supplement” plan covers drugs. TRUTH: If you have a plan (except for the rare instance that you bought it before 1992) that covers drugs, it is NOT a Medicare Supplement plan – it is a Medicare replacement plan (Medicare Advantage). These plans take the place of Medicare instead of supplementing it.

Call Us:(877) 506-3378

Medicare Supplement Plans

The Medigap plans are standardized by the Federal Government, so there is no difference from one company to another. They all must go by this standardized plans chart: Medigap Coverage Chart.

The plans that are offered are:

- Medigap Plan A

- Medigap Plan B

- Medigap Plan C

- Medigap Plan D

- Medigap Plan F

- Medigap Plan G

- Medigap Plan K

- Medigap Plan L

- Medigap Plan M

- Medigap Plan N

Medicare Supplement Companies

There are hundreds of companies nationwide, offering Medicare Supplemental insurance. However, there are only a few that are both competitively-priced and highly-rated. Most of these companies operate in many states. If you request quotes, you will receive information about which companies offer which plans for your specific age and zip code. Some of the primary companies that do business in Medicare Supplemental insurance are:

- Mutual of Omaha Medigap

- Gerber Life

- Central States

- Family Life

- Aetna

- Philadelphia American

- Loyal American

- American Continental

- New Era

- Forethought Life

- Sentinel Security

- Sterling

- Woodmen of the World/Assured Life Association

There are, of course, other companies that sell Medicare Supplements, and as an independent brokerage, we work with the options that are most competitively priced in your particular state.

Other Resources

Here are a few other resources that may be useful to you:

- Medicare’s Website – www.Medicare.gov

- “Choosing a Medigap Policy”

- How to Find Information about your State Dept. of Insurance

- Get a Medicare Supplement Quote

- Medicare informational blog

List of States Served By Medicare-Supplement.US

- Alabama

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montanta

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming